Whereas most investment trusts trade on a discount to net asset (NAV), it’s common for some to trade at a premium – usually driven by a mix of quality, scarcity, sentiment and structural features.

There has a been a shift with this trend as premiums evaporate across the investment trust space. At the end of March, only 15 investment trusts traded above the value of their underlying assets, and the premiums were tiny.

Certain boards might not want their trust’s shares to trade at a premium as it can be a turn-off for investors. But to others, a premium is a sign that a trust has something interesting to offer.

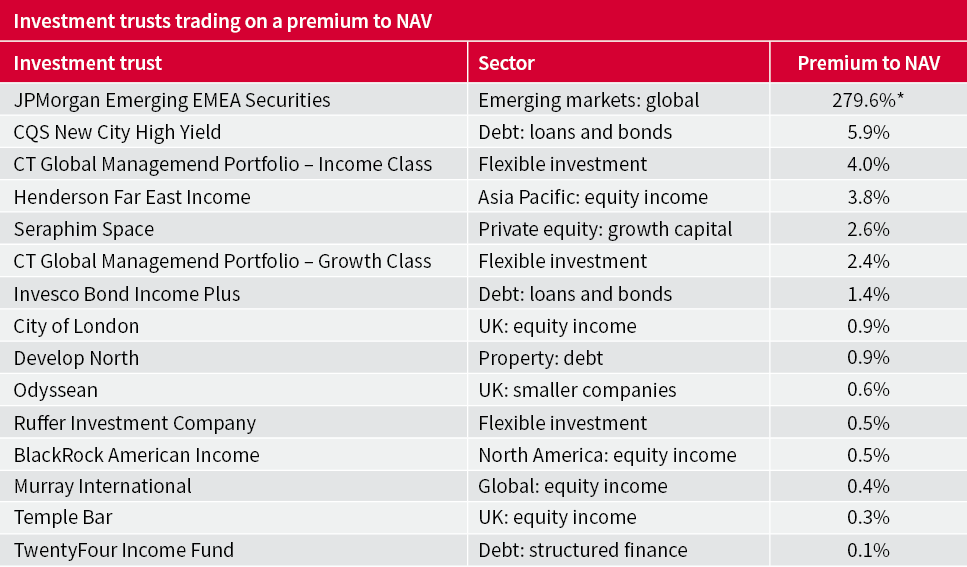

Source: AJ Bell, Winterflood, 27 March 2026. *This is abnormally high as investors are speculating on the value of its Russian assets. They've essentially been written off, but if sanctions were lifted, legal cases resolved, or assets recovered, the potential uplift in valuation could be large.

While it is easy to suggest this is a factor of markets going through a difficult period, there is an argument to say that market volatility encourages more investors to pay up for trusts with a good track record, and so we might expect more to trade at a premium.

When times get hard, investors often lean on fund managers for their experience of investing across market cycles, so in theory they should still be happy to pay a premium for those with a solid track record.

Interest in more defensive style investing also tends to accelerate when markets go through a tough patch, such as we’re seeing now. That explains why Ruffer Investment Company has flipped from a discount as wide as 5.9% over the past 12 months to now trade at a 0.5% premium.

Temple Bar has proved its worth over the past five years with a market-beating performance, and that’s put it on investors’ radars as they seek value-style opportunities in more volatile market conditions. Temple has commanded a premium for most of the past six months, whereas historically it was on a discount.

Infrastructure and renewable trusts used to have widespread premiums thanks to their rich sources of income when yields on cash and bonds were low. They now command deep discounts due to higher financing costs, falling asset valuations and reduced demand for the shares, particularly in the wake of higher bond yields this year.

A shift in market conditions is also to blame for scarcity of premiums. Volatile markets can make investors reappraise what they’re prepared to pay for any investment. We’ve seen this on a broad basis and with specific situations. For example, the S&P 500 has de-rated from 22-times forward earnings to 20-times over the past two months.

Lindsell Train Investment Trust at one point traded more than 60% higher than the underlying value of its assets. Investors were happy to pay a premium as it was the only way they could invest in the Lindsell Train asset management business. The trust owned a stake in the privately held asset management firm, and its lead managers Nick Train and Michael Lindsell for years delivered superior returns to investors.

When the Lindsell Train-managed funds and trusts started to underperform, investor interest in Lindsell Train Investment Trust waned and its premium disappeared. It now trades on a 17.9% discount.

More recently, private equity group 3i saw its premium rating turn to dust. Over the past 12 months, 3i has gone from a peak premium of 69.6% to a discount of 24.2%. That’s a radical de-rating and has been driven by investors losing faith in Dutch retailer Action which dominates 3i’s investment portfolio.

For years, investors were happy to pay a premium for 3i as it was impossible to invest directly in Action, which has been one of the biggest success stories in European retail besides Aldi and Lidl in the past decade.

The premium rating has slowly narrowed in the past six months but disappeared in late March when 3i warned of potential headwinds for Action. A prolonged Middle East crisis could lead to higher interest rates if central banks must deal with an inflation shock, and that is bad news for consumer spending. Action is also having a tough time in France, overshadowing its ambitions to crack the US market.

Other investment trusts to have lost their premium rating over the past 12 months include UK smaller companies trust Rockwood Strategic amid falling risk appetite. Ashoka WhiteOak Emerging Markets has gone from a premium to discount off the back of a strengthening dollar, which creates headwinds for emerging markets. AEW UK REIT has also de-rated amid a shift in interest rate expectations, with the prospect of higher rates in the UK souring sentiment towards property stocks.

It’s also worth considering that the investment trust industry is structurally challenged, as there are fewer buyers in the wealth management space, and retail interest is waning in parts of the market.

Weaker trusts are merging with others or being wound down, while the reputation of active management in general is being challenged by poor performance figures.

Many investors are switching to passive investments for cost and convenience, meaning the overall pool of potential buyers for investment trusts is shrinking.

Many investors are switching to passive investments for cost and convenience, meaning the overall pool of potential buyers for investment trusts is shrinking.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.