As Sun Tzu wrote in The Art of War, “No country has ever benefited from a protracted war.” For the moment, at least, it seems as if everyone’s worst fears regarding the conflict in the Middle East are coming true in so many ways, as the fighting drags on and starts to escalate.

From the narrow, and selfish, perspective of financial markets this is slowing down, if not yet derailing, an equity bull run, and it will be interesting to see whether the latest bout of volatility has any effect upon plans for what are still being touted as three of the biggest initial public offerings (IPOs) in the form of SpaceX, Anthropic and OpenAI.

Each could, in theory, come with a price tag of at least $1 trillion, and at the same time provide the sternest test yet of financial markets’ appetite for all things related to Artificial Intelligence and, more widely, the concept of American exceptionalism, especially in the fields of finance and technology.

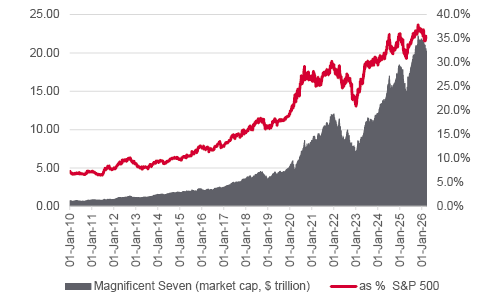

The so-called Magnificent Seven US technology companies – , Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla – , are all among the ten most highly valued public companies in the world. Each has a stock market capitalisation of at least $1.5 trillion.

Between them, they represent 35% of the S&P 500’s total value and, by extension, 21% of the FTSE All-World index.

Source: LSEG Refinitiv data.

There have been similar periods in the past when one sector, or select grouping of stocks, drove US and global equities to new highs. These include the ‘onics and ‘tronics (technology) names of the late 1960s, the Nifty Fifty in the early 1970s and then the technology, media and telecoms (TMT) sectors in the late 1990s. All were very profitable for advisers and clients on the way up and providers of equal amounts of pain on the way down.

Narrow markets are prone to toppling over, as valuations prove stretched, earnings forecasts unattainable, and sellers start to overwhelm would-be buyers, especially when those getting out first are those on the inside, in the form of early-stage finance providers, such as venture capitalists, or management and staff.

This is where IPOs and new stock market listings enter the equation, as a deluge of new floats eventually drowns everyone. It was not for nothing that Warren Buffett once tartly described the process thus: “First come the innovators, who see opportunities that others don’t. Then come the imitators, who copy what the innovators have done. And then come the idiots, whose avarice undoes the very innovations they are trying to use to get rich.”

So far, though, there have been no blockbuster IPOs. Space exploration leader Space X, and AI system developers Anthropic and OpenAI could be about to change that, the war and market conditions permitting.

This is why these deals could be a key test of sentiment for the tech sector and US equities more generally, especially given their putative price tags.

Even if they do not happen, or come with a lower valuation, that could tell us something, but a frenzy which begets more new entrants would be potential red flag.

Not surprisingly, Buffett’s mentor, Benjamin Graham was similarly wary of buyers flocking to shiny, expensive market newcomers just as the smart money crept toward the exit, arguing in his 1934 tome Security Analysis, “One of the most devastatingly accurate of these economic rules is this: anytime the term ‘New Era’ becomes widely accepted, get the hell out of the stock market.”

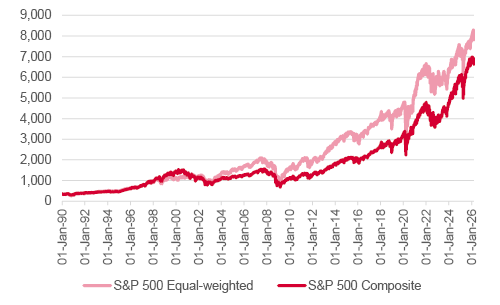

We are not at that stage. But any adviser or client who wishes to keep exposure to the American economic engine, and its entrepreneurial, go-getting culture while managing the risk posed by technology valuations and a top-heavy stock market does have the option of seeking exposure to a version of the S&P 500 that is equal weighted across all of its members, rather than market-cap weighted.

Source: LSEG Refinitiv data.

The equal-weighted version of the benchmark has actually outperformed the actual S&P 500 since 1990, in both capital and total return terms.

The difference in the compound annual returns may look modest – 8.9% a year versus 8.4% in capital returns, and 11.1% a year versus 10.7% for total returns – but over 36-and-a-bit years that adds up to 335 and 613 extra percentage points of performance.

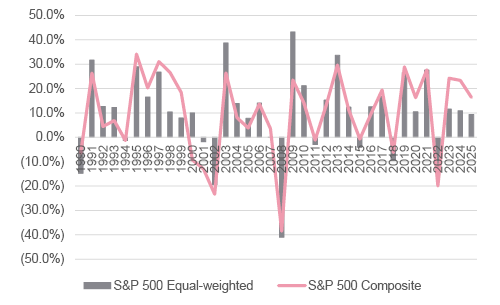

The S&P 500 massively outperformed during the TMT bubble of the late 1990s, but the equal-weighted version helped advisers and clients weather the bust and capitalise more fully upon the recovery.

Source: LSEG Refinitiv data.

Advisers and clients may therefore be intrigued by how the official, market-cap weighted version is again on a multi-year run of outperformance. Whether Space X extends the index’s orbit will be interesting to see, assuming it gets the chance.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.