March was dominated by the outbreak of conflict in Iran, which caused significant market upheaval and brought an abrupt end to what had been a broadly positive start to the year. Rising geopolitical risk had already been a defining feature of the early months of 2026 – first with the US intervention in Venezuela, and then with President Trump's posturing towards Greenland – but the escalation in Iran swiftly eclipsed both to command global attention.

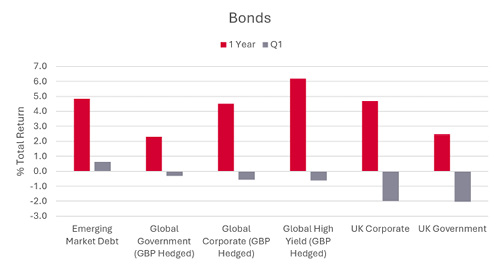

Bond markets have faced a challenging reversal in 2026. Expectations of inflation returning to 2% targets have required meaningful upward revision in light of sharply rising oil prices, and central banks have responded with a notably hawkish tone – moving swiftly to convince markets of their willingness to raise interest rates decisively. This has prompted a broad repricing across fixed income. Whilst the most pronounced volatility and yield rises have been concentrated at the shorter end of the yield curve, it is longer-dated bonds that have delivered the weakest total returns. The UK bond market has been the hardest hit, owing in part to the country's structural reliance on energy imports.

In corporate bond markets, credit spreads have begun to widen from historically tight levels, signalling growing investor caution, though the broader fallout has remained relatively contained.

Source: AJ Bell and Morningstar, As of 31 March 2026. Total returns represent those in GBP terms.

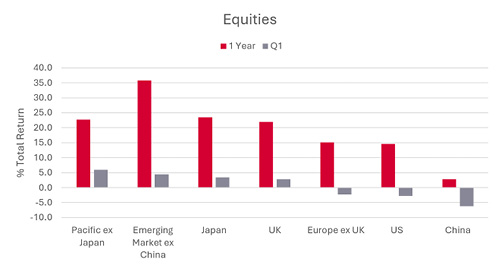

Equity markets have been volatile throughout the quarter, responding to an unpredictable flow of news regarding the trajectory and potential escalation of the conflict. Whilst most markets have felt its effects, first-quarter returns have also been shaped by how individual markets were positioned heading into the crisis.

In the US, a softer start to the year somewhat obscures what has been a degree of relative resilience since the conflict began. Japanese equities delivered strong gains after a decisive election result provided a clear mandate for the continuation of economic reform. Within emerging markets, South Korea has been the standout performer, benefiting from growing appreciation of its role within the AI supply chain. Closer to home, UK equities have outperformed, supported by the market's heavyweight exposure to the energy sector, with the major oil companies buoyed by rising crude prices.

Source: AJ Bell and Morningstar, As of 31 March 2026. Total returns represent those in GBP terms.

As with any event that dominates market attention, the range of potential outcomes is wide and largely contingent on political decisions that are, by their nature, difficult to forecast. Scenarios span from a relatively swift de-escalation – which would provide immediate relief to risk assets and take pressure off energy prices – through to a prolonged conflict that continues to weigh on growth expectations and keeps central banks in a difficult position. The latter would present the more challenging environment to navigate: one in which policymakers face the unenviable task of responding to inflation driven by factors largely outside their influence, whilst simultaneously managing the risk of tipping economies into recession.

In the near term, oil prices are likely to remain the key variable for both inflation dynamics and market sentiment. Beyond energy, however, the conflict has reinforced a broader reassessment of supply chain vulnerabilities, defence spending trajectories, and energy security – themes that are likely to shape investment narratives well beyond the immediate volatility.

For portfolios, this environment underscores the importance of genuine diversification – not merely across geographies, but across asset classes, duration, and the type of risk being taken.

Ultimately, against a backdrop of elevated geopolitical and event risk, ensuring that portfolios are resilient across a range of scenarios – and positioned to deliver an appropriate journey for clients – feels more important than ever.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.